By Dr Charles Ellinas

The energy factor

One of the big problems around the East Med is that governments often talk about developing their gasfields as if they are in full control. As if they are the ones to decide and whatever they decide will be done. Statements like: “we will send our gas to Europe because Europe needs it so that it can ditch Russian gas”, or, “we will bring it to Cyprus for power generation, with the rest to be liquefied and exported,” or “export it to Turkey”, abound.

Governments and politicians talk about East Med energy mostly in terms of their political ends, whatever these are at any one time, blissfully unconcerned about techno-economic factors. In the space of the first eight months of 2023 President Netanyahu promised Israeli gas to Italy, to Turkey and to Cyprus, even though available gas is only sufficient to supply only one of these routes. Chevron, the operator of the Leviathan and Tamar gasfields in Israel, of course has other, commercially driven, plans.

The reality is that while oil companies have an obligation to work with governments, ultimately, they will propose development plans driven by commercial factors and aligned to their business priorities. After all, they foot the bill, they have the required technology and expertise, they take project risk and have the reach to global markets to sell the gas.

What will happen in the future with East Med natural gas depends to a very large extent on the oil companies and not on regional governments. Governments have the power to approve, or not, development plans proposed by the oil companies, but not approving them entails a risk that a project may not progress.

The best approach is to cooperate closely and support the companies to ensure that such plans progress to implementation, if East Med countries are to benefit and not end-up talking again in a few years about missed opportunities.

Cynicism abounds in Cyprus when any optimism is expressed that a project may actually progress. People are right to be cautious and often outright cynical. Many premature promises were made in the past, only to fall by the wayside.

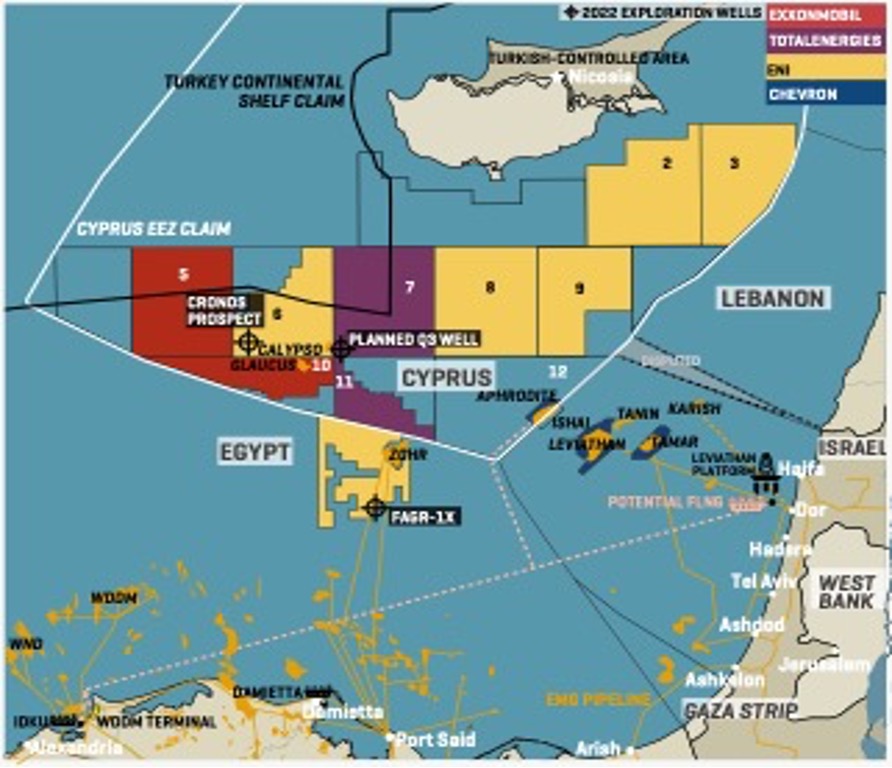

A good example is the potential exploitation of the Aphrodite gasfield. Following successful appraisal drilling, NewMed submitted in May on behalf of its partners Chevron and Shell a development plan for government approval. There were missed opportunities, followed at regular intervals by promises that exports will start by a certain date, only for that date to become a moving target that never arrives. There are reasons to believe that there is now the best chance since 2013 that Aphrodite may actually “re-surface”, but given the politics of Cyprus and the region it is difficult to be confident.

Globally, concerns about energy security, and security of energy supplies, are leading to a re-balance of the trilemma: energy reliability, sustainability, affordability. The push-back has already begun. This includes Europe that is now facing a growing increasing resistance against more policies to address climate change and protect the environment, causing a growing resistance to green policies. These developments will culminate with COP28 in Dubai in December, where the world will have the opportunity decide how and at what pace to move the clean-energy transition forward.

East Med gas to Europe – or not to Europe

East Med political leaders keep talking persistently about sending their gas to Europe because “Europe needs it to replace Russian gas.” But there are two big problems with this. First, Europe’s needs to replace Russian gas are confined to the next few years, and certainly not beyond 2030 – its REPowerEU strategy makes that abundantly clear. The same strategy is targeting reduction of gas demand in Europe by 30% by 2030, and to continue reducing it all the way to net-zero emissions by 2030. Europe actually achieved a 17.7% reduction in the period August 2022-March 2023, compared with the average gas consumption for the same months between 2017 and 2022. This trend is expected to continue next year and beyond.

With such targets the EU is not looking for new long-term gas supplies. The oil companies operating in the East Med have made it abundantly clear that without long-term commitments from EU buyers of gas – for 20+ years – they will not proceed with development of projects solely dedicated to supplying gas to Europe.

It they do, it will be for the Asian energy markets, where demand for gas is forecast to continue well into the future.

East Med developments

Chevron is proceeding in Israel with expanding gas production at Tamar Leviathan, planning an FLNG project to export gas to Asia and to more than double its gas exports to Egypt, that is desperate for new gas supplies because its own production is faltering. Incidentally, given its dire energy situation, Egypt needs as much Israeli gas as it can get, but is also very keen on gas from Aphrodite.

East Med gas-fields

Chevron is going ahead with these plans, despite Mr Netanyahu talking about gas to Italy and from there to Europe and now gas to Europe through Turkey. And in between, the suggestion of Israeli gas being sent to Cyprus, for Cyprus own use, but also for liquefaction and export…to Europe.

As a result, East Med gas development plans often have a longer-term horizon. The oil companies will proceed with gas development projects over time, in response to market opportunities needed to underpin such projects and guarantee long-term, profitable, low-risk sales.

Lebanon is seeing some movement in the energy sector. Even though politically and economically paralysed, on the positive side, following the Lebanon-Israel EEZ agreement, TotalEnergies has commenced drilling in block 9 that includes the Qana prospect. A discovery will transform Lebanon’s fortunes.

This is the right point to mention the perennial East Med Gas Pipeline. Is it still alive? Not likely. It never was. In any case, with Chevron now considering an FLNG at Leviathan there is no sufficient gas to support it. Also Europe is reducing gas consumption now and more in the longer term (see REPowerEU), not looking for new long term supplies.

Associated with East Med’s volatile geopolitics, low-risk is key. The oil companies, and banks, will not invest in projects potentially subject to geopolitical risk over their lifetime.

Solution of Cyprus problem is crucial in this context. Hopefully Tukey’s rapprochement with Greece, Israel and Egypt, and its need of Europe’s goodwill and cooperation, driven by its economic woes, will offer a new opportunity.

Egypt’s desperate need for more gas

Without any new significant discoveries, over the last few years Egypt has been experiencing a steady decline in its natural gas production – as its gasfields deplete – at a time of increasing demand due to its fast-growing population. Coupled with Egypt’s dire economic situation, this is a major challenge, but also a potential security risk.

It has led increasingly to power outages during the summer months, as the heatwave causes demand for cooling to peak. As a result of having to divert more gas for power generation, Egypt has been forced to stop its lucrative LNG exports and will not be able to resume these until October, despite increasing gas imports from Israel.

Egypt’s gas output fell for an eighth consecutive month in May, dropping to a three-year low 5.84billion cubic feet/day (bcfd), about 1.35bcfd below the peak 7.19bcfd achieved in September 2021. This is mostly due to faltering production at the giant Zohr gasfield due to water infiltration problems, with gas production in April about 23% below the field’s production capacity of 3.2bcfd.

Eni has embarked on a repair and drilling programme to increase Zohr’s production, but without new discoveries Egypt’s gas woes are expected to continue.

Egypt is taking measures to limit power outages, including a 20% reduction of gas supplies to fertilizer factories. The Egyptian Electricity Company even issued a warning to citizens, urging them to avoid using elevators at specific times for safety reasons, sparking anger. It should be remembered that energy shortages and power supply black-outs were a major factor in the eventual downfall of Mohamed Morsi in 2013.

At a recent meeting between the heads of Egyptian intelligence and Israel’s National Security Council, Egypt is understood to have pressed Israel to increase gas exports. Recognizing the political and security risk, and the need to have a stable Egyptian government, Israel approved more than doubling gas exports to Egypt. With a price claimed to be close to $7.50/mmBTU, this is also attractive to the gas-producing companies in Israel. Chevron is expanding production at Tamar and Leviathan for this purpose.

Israel uses natural gas exports to enhance its regional status. Something similar could also benefit Cyprus. Such exports would strengthen its relationship with Egypt, especially as the country is in desperate need for more gas – provided of course that its dire economic situation does not affect its ability to pay for such gas.

Impact of climate change

With the impact of climate change visible all around us, and uncertainties in global energy policy and direction continuing, Europe, the US and the UN are pushing for a faster energy transition. COP28 in December is expected to add to the urgency.

The East Med is not immune to this. The window for developing its gas is closing fast. The region must prioritize development of renewables from the currently low levels. Upgrading electrical grids, electricity storage and the construction of electrical interconnectors can help hasten the uptake of green energy. This must be the new priority. The East Med can then utilize its natural gas regionally, in support of RES during transition.

To access the PDF file on the ‘DergiPark Academy’ website, please follow these steps

To review other articles in Replete Issue 18

Dr. Charles Ellinas

@CharlesEllinas

Senior Fellow

Global Energy Center

Atlantic Council